Artificial intelligence (AI) dominated technology investment discussions in 2023 and is poised to maintain its allure in the upcoming year. AI has significantly reshaped the financial landscape, transitioning from a novel concept to an established technology. Projections by GlobalData estimate the AI market will reach a substantial value of $908.7 billion by 2030, signifying an enduring impact and potential growth across industries.

Although a transitional period is necessary, AI is expected to shape a promising future for fintech, introducing fresh value to the industry’s business and customer facets. Notably, the surge in generative AI (GenAI) technology continues to be a driving force, influencing every sector. GlobalData’s predictions indicate a remarkable growth trajectory for the GenAI market, expected to soar from $1.8 billion in 2022 to an impressive $33 billion by 2027, demonstrating an outstanding compound annual growth rate (CAGR) of 80%. This reinforces the transformative power of AI, shaping the future of fintech and beyond.

AI’s Big Challenge: Managing the “Threat”

Risk management is already part and parcel of fintech. The prevalence of private and customer data and the high stakes in financial exchanges make risk management ubiquitous. Up until 2022, total fraud losses had steadily increased.

In 2022, traditional identity fraud losses amounted to $43 billion, marking a notable decrease of nearly 17% from the previous study period. Apart from the decline in dollar losses, the number of U.S. adult victims fell by 2 million, with 40 million individuals affected. This tendency in loss figures reflects the continuous and steadfast efforts of the financial services industry to thwart criminal activities.

While the financial sector has made progress, criminals persist in their tenacity, targeting victims not only through traditional identity fraud but also by exploiting identity fraud scams. That means criminals are getting smarter, and much of that may be due to their leveraging increasingly advanced technologies, including AI.

Tracking identity fraud scams as a standalone category since 2020 has provided a more detailed and nuanced understanding of identity fraud in the United States. Although strides have been made, there is still substantial work to be done to diminish the impact of identity fraud across the industry significantly.

Addressing the Threat

The integration of AI in fintech has presented an ongoing challenge, prompting individual financial institutions and regulatory bodies to continuously explore effective strategies to navigate and harness the capabilities of AI.

How exactly does AI act as a ‘threat’ in fintech? They vary from low-risk scenarios to highly problematic ones. On the low-risk end, one can imagine a chatbot in a CS use case “tricking” a customer into thinking it’s a human being. High-risk scenarios might involve violating a customer’s basic rights to privacy or using AI-enabled manipulation techniques to influence financial decisions.

The European Union has implemented measures to address potential risks associated with AI in fintech. The draft regulation, known as the AI Act, seeks to guarantee the safety and adherence to fundamental rights and EU values for AI systems introduced to the European market and utilized within the EU.

This groundbreaking proposal not only prioritizes safety but also endeavors to foster investment and innovation in the field of AI across Europe. The introductory rules established by the governing body represent early regulations globally, shaping the usage of AI in the financial services sector.

Amid ongoing discussions surrounding the EU’s proposed AI regulations, RegTech firm Saifr has emphasized the significance of a risk-based approach. This approach, aimed at fostering innovation, prioritizing safety, and maintaining a robust financial ecosystem, is considered pragmatic. Saifr acknowledges the diverse applications of AI across various industries, with a specific focus on the financial services sector.

The proposed framework involves categorizing AI systems according to their risk levels, ensuring a nuanced evaluation ranging from minimal to unacceptable risks. This approach reflects a comprehensive understanding of the multifaceted implications of AI in different sectors.

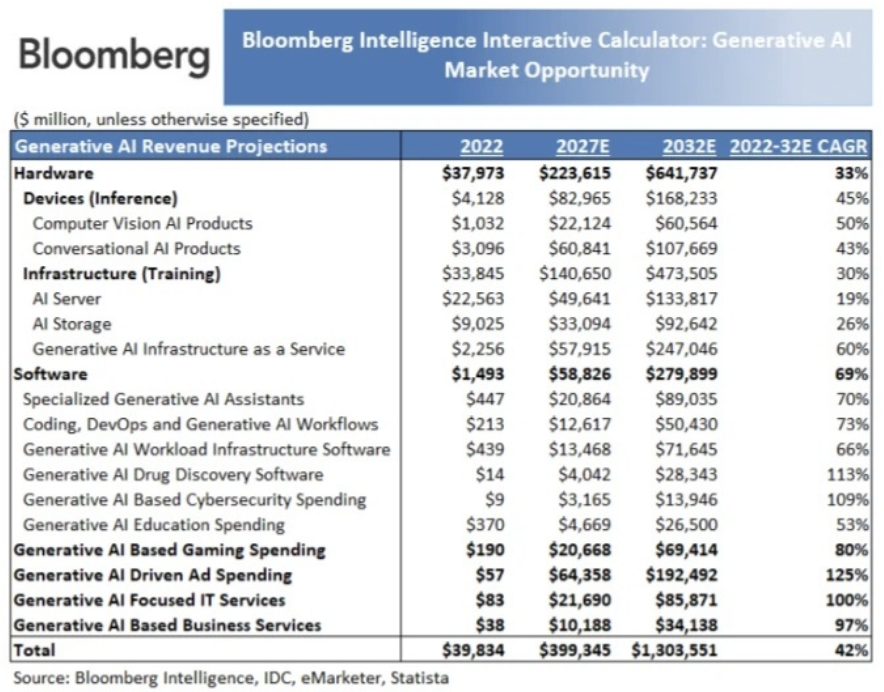

Market report

AI as a Social Entity

An interesting subcategory of risk related to AI at large and AI in fintech is that AI may actually end up functioning as a biased entity in our society. Why is this? For one, those biases already exist in the data the AI parses. Additionally, algorithms are, by nature, discriminatory because they are designed to identify categories and filter out based on unwanted criteria. As Dr. Garfield Benjamin, a researcher at Solent University looking into AI as a social entity, put it, “The whole point of algorithmic decision-making is to discriminate – to judge people according to certain criteria like where they live, their age, their occupation.”

What has already been seen with AI is that this tendency has created a social bias in certain use cases. A recent study published in an international partnership between universities in the U.S. and South Korea established that social biases, including racism and sexism, are already defined within robots that leverage AI.

Consider this scenario: AI is deployed to promote specific financial products to distinct groups. A biased AI might inadvertently exclude marginalized groups from accessing these products, a situation reminiscent of past incidents in the social media realm, where women and African Americans were excluded from advertisements for higher-value products.

Angle Bush, the creator of Black Women in Artificial Intelligence, cautions that the use of AI systems in determining loan approvals poses a risk of reinforcing biases embedded in historical data used to train the algorithms. This may result in automatic refusals of loans for individuals from marginalized communities, exacerbating existing racial or gender disparities.

Another example of AI biases is this: U.S. police departments are increasingly adopting predictive policing algorithms to forecast potential crime hotspots. However, a significant issue arises as these algorithms are shaped by arrest rates, creating a disproportionate impact on Black communities. This, in turn, prompts intensified policing efforts in these communities, resulting in concerns about over-policing. Such situations raise profound questions about the ability of self-proclaimed democracies to resist the transformation of AI into an authoritarian tool.

As rules and regulations continue to develop around AI in fintech, vendors and regulating bodies alike will need to ensure that protections against discrimination exist, ensuring a fair financial landscape for any human interacting with AI-driven products.

Malicious Use of AI

Since the advent of the internet and digital applications, cybercrime has been a central threat to the fintech space. With AI in the mix, these malicious incursions are getting even more complex.

One way AI aids malicious incursions is by adding new levels of complexity to traditional techniques used by hackers. This was recently the case in Arizona where a false kidnapping phone call induced moments of distress for a family, as a mother received a ransom demand for the release of her purportedly kidnapped daughter. The voice on the phone mimicked her child exactly, but it was later revealed to be an AI-generated deepfake.

Contrary to the alarming scenario, the daughter was safe and nowhere near the kidnapper. The family was able to avert any financial loss by taking the appropriate action of notifying law enforcement. They continued to engage the scammer in conversation while simultaneously locating the daughter.

AI-based tools have also started appearing in crypto, impacting trades and markets. To counteract these malicious incursions, financing institutions will need to leverage their own AI use cases as early as they can in the digital banking lifecycle. AI will speed up the threat identification process, replacing human-driven, manual work. Potential use cases include leveraging AI-driven systems to:

- Speed up verification checks and enhance KYC measures.

- Enhance screening of clients against watch lists.

- Engage in more effective transaction monitoring to identify incursions early in the cycle.

While AI has malicious applications, fintech can gain the upper hand by implementing its AI-driven protections as soon as possible.

The Fintech Customer and AI

Now, on to the positives. One significant highlight in the future of AI in fintech is how much value it will bring to the customer experience. Artificial intelligence is positioned to extend a never-ending list of solutions that streamline the customer experience and give fintech companies a competitive edge when it comes to customer service.

As will be explored in greater detail below, one immediate and personal way AI will touch the customer in the fintech space is through the chatbot. AI-driven chatbots will be a first line of defense for customer service departments, efficiently triaging cases and funneling them as needed to human CS agents.

The onboarding experience will be shorter and easier for customers with the integration of AI. AI will streamline customer verification, making opening an account much faster for the average consumer. Finally, AI’s efforts against malicious attacks will provide financial customers with an additional and powerful line of protection against a range of incursions, including data theft.

Fintech’s Future with AI

The future is bright for AI in financial services if fintech firms take the right actions and implement them now. This technology will drive a massive increase in opportunities and revenues. The banking sector is poised to harness significant opportunities in AI, with McKinsey & Company forecasting one of the most substantial potentials.

According to McKinsey Global Institute’s analysis of 63 use cases, generative AI has the potential to contribute an annual value ranging from $2.6 trillion to $4.4 trillion to the banking industry, for example. Below are just some of the ways in which that will happen.

Innovation Through Software Development

Fintech companies looking to ride the wave of AI as their use cases increase in the space will benefit from partnering with seasoned software development companies. We at S-PRO have already begun exploring multiple areas of digital transformation in fintech and other data-sensitive, data-rich industries such as healthcare and energy. Our Fintech and AI software development services allow for fintech companies to develop bespoke solutions that answer directly to their business needs and customer demand.

How AI-Driven Chatbots Will Accelerate Fintech

Chatbots will be central in this new future in fintech, impacting the customer experience at several points in the customer cycle. Chatbots will bring an automated conversational component to websites and applications, messaging interfaces, social media, and voice assistance. Gartner, Inc. predicts that by 2027, approximately 25% of organizations will shift to using chatbots as their primary customer service channel, allowing businesses to deepen customer engagement.

AI-driven chatbots will be able to introduce hyper-personalization into the CS mix, leveraging a customer’s native language, introducing complex financial topics in an accessible and friendly way, and creating a more comfortable space for customers in general. These bots will also take on a range of automated tasks at a financial institution. Everything from resetting a password to executing online payments can be overseen by a “friendly” chatbot that efficiently guides the consumer through a process.

The Trends on Deck

Given the opportunities on the horizon, what are some of the trends gaining momentum in AI in fintech? Let’s walk through some of the highlights.

Predictive Analytics

Making the best financial decisions requires analysis of data. Now that AI is on the scene, fintech development firms can develop solutions that leverage predictive analytics to drive better financial decisions for their customers.

How would this play out in the real world? As part of an online banking app, a financial institution could leverage AI-driven analytics to push out suggestions to consumers. For example, the AI could analyze a customer’s spending habits and make recommendations. This would not only impact a customer’s daily financial decisions but also longer-term goals related to savings and retirement.

Generative AI

Another trend positioned to make a big impact in fintech is generative AI. Generative AI leverages AI and ML to parse data, generate insights from that data, and then push out operational decisions to the C-suite. A CIO at a fintech firm could use this technology to suggest solutions that will better drive revenue growth, according to VP Moutusi Sau of Gartner. Additional fintech use cases include using generative AI in detecting fraud, building risk factor models, and predicting trade trends.

Increased Automation

Manual processes and analog workflows have been a problem in the finance sector for decades now. Perhaps no other industry has stayed married to the analog for as long as finance. AI used in tandem with RPA, or robotic process automation, will go a long way toward eliminating the manual in the space. AN RPA is a collection of bots that execute repetitive workflows and then transfer the information to human staff, who can then review the tasks and approve them more efficiently.

AI-Driven Investments

Brokerages have long been tasked with finding innovative and consistent ways in which to make financial recommendations. Toeing the line too closely leads to minimal returns, while bold moves can expose customers to risk. With AI-powered tools, financial advisors can now provide data-driven, algorithm-based advice to their investors. This will mitigate exposure and risk while also streamlining the entire process.

Improved Authentication

Finally, and perhaps most importantly, AI is ideally positioned to enhance authentication in financial transactions. Previously, the authentication process involved multiple factors, creating a long and arduous workflow. With AI-driven solutions, authentication can now take just a fraction of the time by leveraging digital data such as scanned iris images or fingerprints. Financial institutions will be able to onboard new customers much more quickly while also protecting themselves from KYC violations and fraud.

Regulatory Compliance

Fintech companies face the ongoing challenge of staying compliant with dynamic financial regulations. AI emerges as a key solution, streamlining compliance checks and reporting and aiding adherence to regulations while optimizing time and resources. The integration of AI in regulatory compliance is anticipated to enhance fintech’s ability to navigate the intricate regulatory landscape in 2024 and beyond.

Anticipated future developments include AI-driven solutions for regulatory compliance, such as predictive models assessing the risk of violations based on factors like customer behavior and transaction patterns. These innovations may empower fintech firms to implement more robust compliance programs.

AI’s role extends to identifying and mitigating risks effectively, safeguarding consumers and investors from fraud and financial crimes. Moreover, by automating compliance tasks, AI allows fintech companies to allocate resources to strategic initiatives, fostering a more efficient and secure financial ecosystem.

AI – a Future of Innovation for Fintech

The next several years will be interesting as fintech companies, financial institutions, and banks navigate a new technological terrain with AI. At the governmental level, policies will continue to evolve in real-time as regulation tries to keep pace with developing tech. From the business side, any entity in fintech needs to begin exploring their options, making AI work for them instead of against them.

Partnering with software developers such as S-PRO is the best way forward. We develop solutions that leverage AI dynamically, improving workflows, enhancing security, and streamlining the customer experience. Whether the starting point is a chatbot or a full-service platform, start exploring how a company like S-PRO can help your fintech endeavors stay ahead of the curve. Contact our team today to learn more about how you can innovate a new AI-driven future for your company.

Subscribe

Thank you!

Get ready! You will receive handpicked content right to your inbox.