You can read the first part of this article here. For those who for some reason don’t like to follow the links, let me remind you briefly: in the first part, we made a retrospective of fintech trends in 2020 and delved into the first 5 trends in 2021.

So what in my opinion awaits us next?

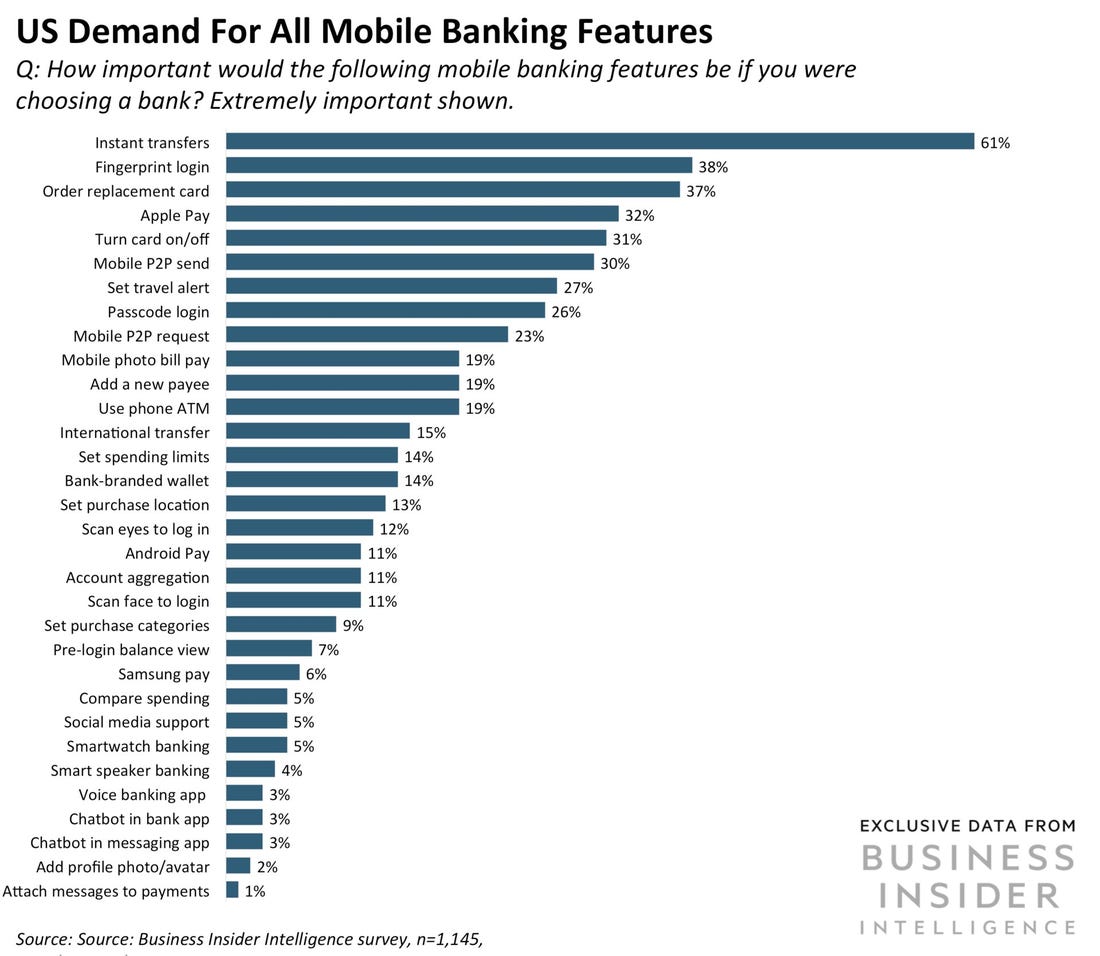

6. Hyper-Personalization in banking

Banks are moving into the segment of sales of packaged digital products and personalize various services for customer needs. For example, a personalized financial plan for a young couple, for a student, for older people, and so on.

Hyper-personalization in banking gives users more flexibility in products and services. For example, based on the relationship with the bank, credit standing, and asset base, the bank recommends to clients how they can design a loan to fit their needs. The customer chooses one of the provided interest categories, duration, payment schedule, and the amount of the first instalment.

To hyper-personalize its services, banks must collect and analyze data from many different sources, including all types of interaction with the customer. Analyzing this data and creating insights allow banks to hyper-personalize the interaction into a holistic relationship, which drives differentiation and increases customer loyalty.

If the bank can sell a complex product that will be convenient and efficient, then there is the question of interaction between banks and other companies (gyms, shops, etc.). Therefore, this requires some flexibility.

Building Customer Loyalty in Digital Banking

7. Banks are becoming more open and automated, building a distribution network

BaaS (Banking-as-a-service) is an industry based on open banking APIs that allow banks to lend their license and infrastructure to technology companies. Leasing banking infrastructure (license, payment processing, card issuance, compliance), instead of creating or buying it for other players, is an extremely new phenomenon but rapidly gaining momentum with the growth in the number of fintech startups.

We are working with a startup in Africa that recently participated in the Ecobank program. Ecobank has made a Sandbox for startups, where you can simply register, access the bank’s products (lending, card issuance, etc.), and later become a reseller of these products. The algorithm is as follows: you register a startup, register with Ecobank, receive an API for the bank’s products, integrate your product with the bank and use it. From the banks’ side the following things are happening: standardization of API, provision of platforms for product testing (Sandboxes), creation of a platform for integration, and control of their products resale process. So, such a technologically complex process is taking place.

Key Things to Know Before Developing a Mobile-Only Banking Application

8. Strengthening automation in investment funds

This is a long-running story, I would say. Many investment funds offer their financial trading services not through a broker, but a program. They create a trading strategy, base the program, and the bot trades on that financial strategy. Apparently, this will intensify. Trade strategies are quite clear, as is the mechanism of their automation. And so in the future more and more players will do it.

At the same time, the entire financial market is being digitalized. If there are clear metrics that will drive the financial market (and they obviously are), then within this you can put a trading strategy in the program and trade. And this process can be correlated – to make risky strategies or not. At the same time, there is hedging, a risk insurance mechanism. A person, knowing that the bot is trading, hedges and gives % of the profits to the insurance company, which covers losses in case of bot’s loss. It’s also convenient for the investment fund because there is no need to hire additional people. Instead, they hire programmers who improve these financial strategies.

9. Growing demand for expertise in software development: working with Big data and high-load systems

Fintech companies need to work closely with developers, designers, and technicians to ensure that all new ideas and concepts are properly implemented.

After all, this is the industry with high-load projects, so it needs expertise in Big data or high load systems. There are many analytics and data preservation issues because it’s working with financial information. How will this affect the outsourcing and software development market? First of all, people with the right thinking approach are needed, because fintech has a demand for transformation. Transformation is about people who can think differently. Secondly, there is a request for quality service.

Summing up, I think that outsourcing companies need to hire the right people, focus on project management, and there must be a clear delivery mechanism. And for sure, it is extremely important to ensure a sufficient level of security.

“Transformation is about people who can think differently.”

What Things We’ve Learned at Machine Learning Prague 2019

10. Pandemic adaptation: remote presence and localization

Two contexts are emerging against the background of the COVID-19 pandemic. The first one is the localization of people in their work, especially in their offline activity. If before everything was moving towards globalization, now there is a trend of remote work and presence, including financial management. The second one is that companies need to work online and interact with their customers and employees remotely. At the same time, they need to have some local presence and to improve the customer experience for all their clients with an emphasis on remote work.

Microsoft conducted a survey of 9,000 employees and business leaders in 15 European countries to learn about their remote experience and future expectations. The changes have been significant: if last year only 15% of companies had a flexible work schedule, now 76% work that way. It turned out that even after the pandemic, neither managers nor employees want to return to the old ways of doing business.

According to the study, Microsoft has developed guidelines for employers seeking to unleash the full potential of remote teams and teams with mixed work schedules. You can find more information in the Microsoft blog.

Coronavirus for businesses: a disaster or a tremendous opportunity?

Conclusion

In summary, let’s systematize the forecasting trends separately for B2B and B2C.

Most of the B2B products we make are data products when the data from one company are transferred to another one. In the field of lending, for example, it is the scoring of loans and their resale. I can say that the big fintech trend in 2021 for B2B is the development of products that provide data analysis.

According to B2C, it’s the digitization of banking services for the population, mobile banking and hybrid services to improve the customer experience. The big fintech trend in 2021 for B2C is the development of various customer experience products, onboarding products, and KYC-services.

Even after life returns to its usual, “non-pandemic” state, some of the behaviours started by the pandemic will continue, including those that intersect with financial technology. And this is for the better because the crisis has forced the industry to adapt to new conditions, look for new opportunities to reach users, and thus – to provide them with more comfort and benefits from the use of fintech products.

Subscribe

Thank you!

Get ready! You will receive handpicked content right to your inbox.