You might have thought about how to start a bank. These financial organizations are not easy to launch as they are heavily regulated and scrutinized.

There are many legal hoops to jump through before you can open a bank. Typically, it takes bank founders well over a year of regulatory compliance and administrative work before they can even take their first deposit.

This is because banks are some of the most important institutions in a modern economy.

Their job is to keep money belonging to depositors and to lend money to clients who need it. They also help businesses run, meaning they give an economy the liquidity it needs to function.

This article will show you what is required to start a bank business. It will cover the most important factors as follows:

- The overall requirements

- The business plan

- What the founding team needs

- What regulations must be followed

- Capital requirements

- Understanding the core banking system

Introduction: The Evolution of Banking in 2026

Choosing to start a bank is always a complex endeavor. In today’s high-tech world, it also comes with some unique requirements. Bankers always had to contend with regulations and legal requirements that dictate how to run a bank and what it needs to stay compliant. But, nowadays, that is also compounded with a whole slew of technological additions.

The digital transformation has well and fully arrived. There is already talk of AI-powered banks out there. Some current trends center around technology, so starting a bank will require a solid team of engineers. For example, you will likely want to rely on cloud providers to store information, run your internal systems, and create disaster recovery plans.

While fully AI-powered banks are unlikely to emerge this year, general use of AI is possible in banking. For example, AI helps with fraud prevention, risk assessment, and customer management. However, it’s important not to overhaul classic systems fully, as Deloitte’s report mentions that the banking business is prone to suffering from “change fatigue.”

Still, as you now understand, if you want to own a bank, you will have to use technology to its fullest potential, in addition to entering a market that is already booming. However, there is still space for new players to make their mark. The main question now is how you build your banking operation, and that’s what this guide is here for.

Figuring out how to start a bank business today looks completely different than it did two years ago. The industry moved past building isolated financial applications, turning instead toward ecosystem models. The Next age of fintech | McKinsey report notes that fintechs achieved an NPS 2.5 times higher than traditional European banks and generated $650 billion in revenue. Yet, they still hold only about 4% of the market. This gap leaves plenty of room for new entrants. However, if you plan to start a bank, you must own the entire customer relationship, rather than just plugging into underlying payment pipes.

To capture that relationship, founders frequently ask:

How much money do you need to start a bank?

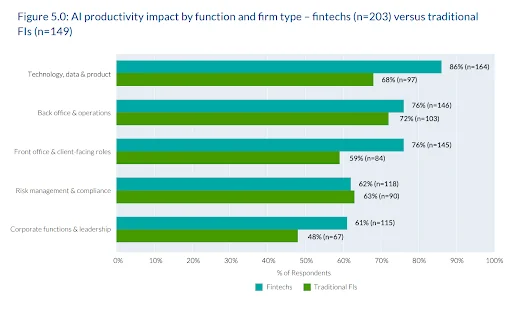

But capital alone cannot buy modern technical agility. In fact, artificial intelligence completely rewrote these requirements. We dropped rigid chatbots for agentic AI integrated directly into core infrastructure. The 2026 Global AI in Financial Services report notes 79% of institutions see tangible gains from embedding generative AI into operational flows. This shift strips away back-office lifting, accelerates support, and lowers barriers for credit products. Consequently, user interfaces changed; customers now expect intent-driven interactions happening naturally through conversation.

The report also shows that AI gains are already visible across the functions that matter most for modern banking: product, operations, customer-facing roles, and compliance.

However, this rapid deployment of automated intelligence carries a steep security cost. The industry experienced a massive spike in synthetic identity theft, as detailed in the Identity Fraud Report by Sumsub, where coordinated rings replaced simple scams with complex attacks. Advanced transaction monitoring now forms your foundational architecture. Without machine-learning-driven anomaly detection, a new platform cannot pass regulatory audits. Today, how you start a bank depends as much on what you do to prove trust as on the code you ship.

Balancing these heavy security barriers is tough, especially since consumer patience is wearing thin. People demand deep personalization but crave ultimate control over their funds. Current data from the Top Banking Trends 2026 by Accenture reveals that 71% of users want AI assistants built directly into banking apps. Interestingly, 82% of them still want the final say when confirming automated actions. This delicate balance between algorithmic speed and human autonomy dictates exactly how modern platforms function.

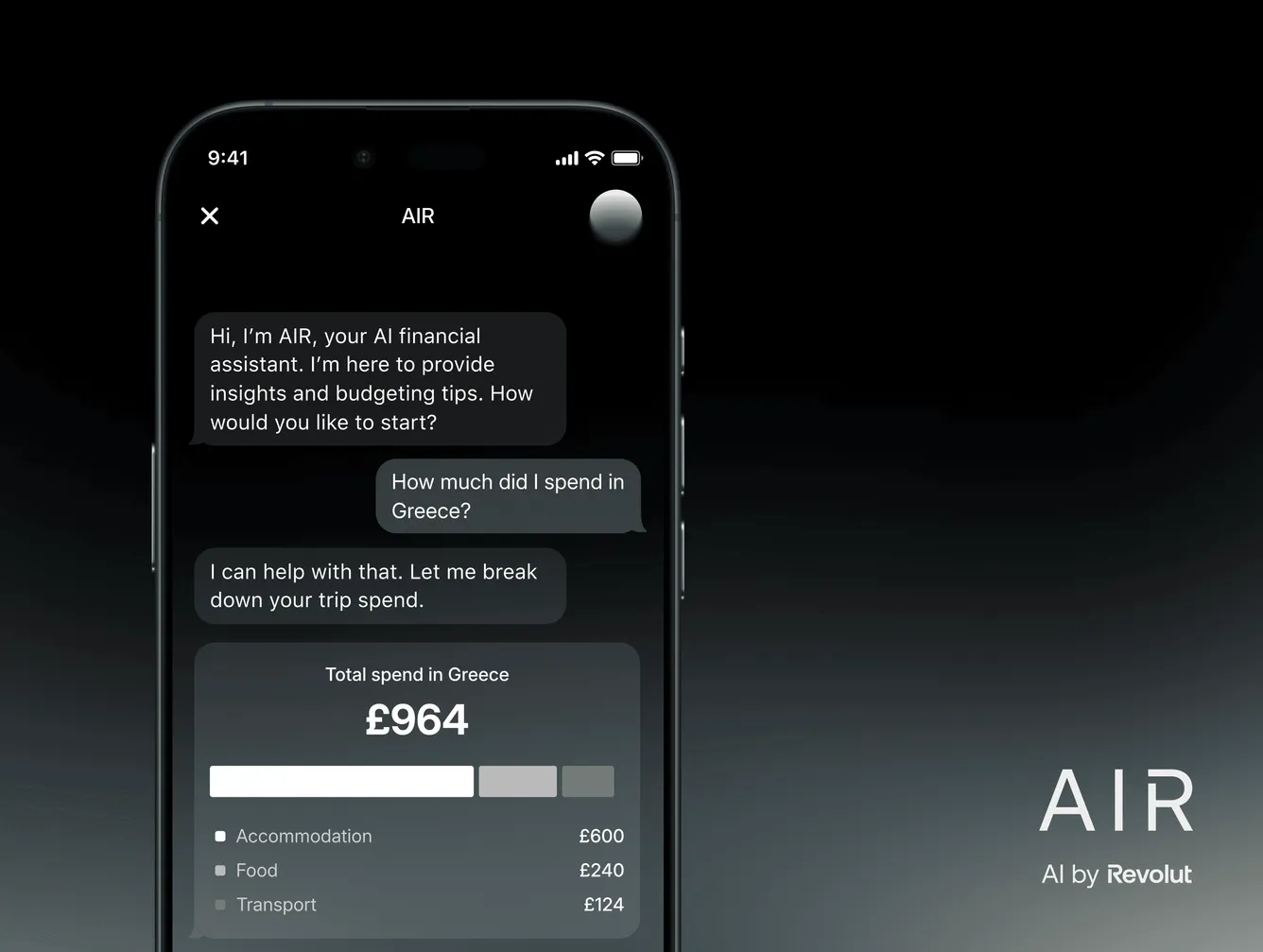

Revolut perfectly illustrates this balance in practice. They officially launched AIR, their in-app AI assistant, acting as a conversational financial manager rather than a simple helpdesk. Users can break down spending habits, freeze cards, and buy eSIMs just by chatting. This move highlights the transition away from static screens toward interactive financial management. Ultimately, to successfully start a bank in 2026, you must build an intelligent, secure, and reliable financial companion.

Minimum Capital Requirements to Start a Bank in 2026: How Much Do You Need?

If you’ve decided to start a bank, you’re probably already expecting to spend a great deal of money. However, everyone has their metrics, and it’s important to try and clear up just how much this venture will cost.

For the US, official requirements state that a national bank must have the following minimum capital ratios:

- A common equity tier 1 capital ratio of 4.5 percent.

- A tier 1 capital ratio of 6 percent.

- A total capital ratio of 8 percent.

- A leverage ratio of 4 percent.

- For advanced approaches national banks or Federal savings associations or, for Category III OCC-regulated institutions, a supplementary leverage ratio of 3 percent.

- For Federal savings associations, a tangible capital ratio of 1.5 percent.

These latest requirements were released in August 2024 and could change over time but will likely remain relevant. So, starting a bank in 2026 does require running some calculations. Chiefly, you need to see how you will distribute your starting investment and whether you meet the necessary qualifications based on the ratios.

There are also other finance-related regulations for those who wish to own a bank, such as getting explicit permission from two legal authorities. You’ll also need to prepare lots of documentation regarding the bank’s business plan, senior staff, risk management, etc. As a result, you will be spending both time and money on getting all this together.

So, in short, a banking business requires a lot of capital to start and you will have to move it around to fulfill specific capital conditions to fulfill the latest FED regulations.

Dustin Schulze

Senior Business Analyst

Ready to launch your own digital bank?

Get expert insights from Dustin Schulze, Senior Business Analyst at S-PRO. With 10+ years in fintech, Dustin guides you through strategy, compliance, and tech essentials to turn your idea into a fully operational bank.

What you need to start a new bank

With so many banks already in operation, you might think starting a bank is easy. It’s not.

Even in the world’s biggest economy, the United States, only 20 new bank applications are made each year, according to private advisory firm Carpenter & Company.

Meanwhile, in the UK, since 2013, there have only been 4 new banks approved per year on average.

It’s such a big undertaking that many founders seek the help of outside experts and consultants to take them through the process.

Banks are heavily regulated and you will need the green light from multiple regulatory authorities, depending on your location.

Part of your representations will include comprehensive information about the founders, such as:

- Their history and expertise

- Their financial standing

- Whether they have enough capital

- How they intend to handle risk management

- A rock-solid business plan

The capital required is significant. The amount differs per regulator, but common consensus is that $15 million is a good amount of capital with which to start a bank.

Applicants who are not prepared will most likely fail.

Many investors are attracted to the relative safety of banks because they are often stable and deal with many loyal clients. This is because banks are so well-regulated that the prospects of failure after launching are reduced.

Such an appealing investment might attract speculators, but they are quickly discouraged when the difficulty of the process becomes clear.

The importance of the business plan

One of the most important parts of starting a bank is creating a comprehensive and strategic business plan.

The business plan is meant to convince regulators that the bank is a viable venture. It can also be used to attract investors.

The business plan will ideally cover the strategic aspects of the plan, as well as leading into the detail of how the bank will be run on a day-to-day basis.

Here are some of the strategic considerations of the business plan:

- What type of bank will it be – commercial, retail, or a combination?

- What is the structure of the leadership team?

- What is the experience of the leadership team?

- What are the prospects of success based on research-based market analysis?

After detailing the strategic direction of the bank, the applicants should answer some questions about the everyday running of the bank.

This could include highly detailed financial projections and scenario planning down to the finest detail.

The business plan will take into account the cost and timeline of achieving regulation, as well as showing clear plans on how to raise the capital required.

The best business plans normally look several years into the future. Here are some of the finer details the business plan will answer:

- Startup costs of the bank

- Target market and ideal customer

- Name of the bank

- Fee structure for client tiers

- Revenue earning model

Different regulators will call for slightly different information. But most, if not all, of the above information will be requested in comprehensive detail.

The founding team must be strong

Banks can only be founded by people with strong experience in the financial world.

Starting a bank is different to starting a general business where entrepreneurs with no prior experience can be successful. Regulators will not approve a team made up of non-specialist business people who are trying to start a bank. The risks are too high.

To receive a banking license, the senior management team needs to be made up of experienced people with proof of success in the banking world.

Ideally, the board of directors should be made up of subject matter experts who can fulfil a function that will benefit the new bank.

This means that not only must the leadership team have banking experience, but it must have members who can each own a functional area such as compliance, IT, or operations.

It’s not only regulators who place great emphasis on the makeup of the leadership team. Investors will be much more inclined to fund a team of proven experts than total newcomers.

Once you have started your bank, you will find that your team has a great role to play. Unless you are fully funded, which is rare, you will need to remain cost-effective.

Therefore, having internal experts will always beat outsourcing a key function such as compliance or software.

Regulation is key

Regulators in different geographies have their own rules. But one thing is clear: getting a banking license is not an easy task wherever you apply.

There are several legal and regulatory hurdles a bank must clear before it can be given permission to operate. In certain countries, there is normally one oversight body that grants the banking license.

However, regulation works in tandem, and sometimes a different oversight body must also give a separate approval before a bank can operate.

One example of this is in the US, where receiving a State Charter to open a bank is not enough to start operations. A new bank must also secure deposit insurance.

Here are some of the concerns that most regulators will be trying to lock down:

- Ensuring the safety of banks through compliance

- Fostering effective competition between industry players

- Ensuring the protection of consumer rights

- Maintaining the integrity of the financial system

Many regulators ask new applicants to approach them during what is known as a pre-application stage so the regulator can make the application requirements very clear.

However, regulation does not end once a bank has been granted a license. It must sign up to a range of legislative instruments and bodies to ensure it upholds the strict standards of the global banking system.

Banks must subscribe to some, if not all, of the additional regulations:

- Company good practices, including taxation

- Consumer safety

- Anti-money laundering

- Electronic data safety and security

- Fair trading

- Reporting standards

- Conflict of interest declarations

- Investor transparency

- Client securities

- Central Bank legislation

- Know your customer

This might explain the rise of neobanks such as Simple, Moven, and MonoBank.

To avoid many of the regulatory hurdles, these companies have not pursued their own licenses, but instead operate under the licenses of larger, more established banks.

The downside is that in many instances, they cannot refer to themselves as banks, but rather, fintech companies.

Another way to remove the administrative burden of starting a new bank could be to purchase a small bank. However, this is not as easy as it sounds because the process of transferring ownership is also onerous and time-consuming and does not improve the time to market.

New bank applicants must satisfy regulators that they have enough capital.

If they do not have all the capital they need by the time they meet the regulators, a realistic capital raising strategy should be laid out in the business plan.

Bank founders soon realize that raising money for their venture is an ongoing process. New applicants are often advised to not wait to secure all the funds before approaching the regulator.

Sometimes, securing a banking license is enough to secure fresh money from investors who realize how serious you are.

The regulator will indicate what the correct capital adequacy requirements a broker must comply with in order to operate in its market. These capital guidelines are not based on guesswork but are linked to the money required to support the bank’s risk profile, type of operations, and growth ambitions.

New banks will normally need to keep these capital levels in place until its operations become well established and profitable.

As mentioned, new bank owners are advised not to wait to raise all the capital required. The founders of Arival Bank can testify that fundraising never ends. Even before applying for a banking license, they raised $1M from venture investors. This was mostly used for operating costs in the first year. The money was spent on expenses such as salaries, legal costs, compliance consultants, and the initial payment for the core-banking system.

Anything after that was aimed at the bank’s capital and other expenses such as developing the product suite and customer support. Every new founder has dreams of disrupting the market and making waves in the industry, but in the early days, getting the simple things right are important:

- What type of bank are you?

- How much money do you have?

- Do you understand your customer segment?

- Are you set up to make a good impression on the regulators?

The importance of the core banking system

For banks, one of the most important parts of its infrastructure is the software that will underpin its day-to-day functions like deposits, withdrawals, and financial history. This underlying technology is known as the core banking system.

This software is the backbone of a modern bank. It facilitates the record keeping of client accounts, processes financial transactions, records the movement of funds inwards or outwards, and provides an array of reporting options.

It goes without saying that this system needs to be robust and failsafe.

Regulators are keen to know that the core banking system is run by a reputable and trusted system. Not many banks have chosen to develop proprietary core banking systems because of the high cost and ongoing maintenance requirements.

Many new banks purchase white label solutions that are pre-configured.

The white label option comes with the risk attached to any third-party interface. Common concerns are that there could be faulty code in the system that affects the integrity of the bank’s transactions.

Banks must consider if they should write their own code from scratch. But writing robust code is not as simple as it seems, mainly because as the bank’s line of products grows and develops, so does the work required to maintain the code.

New bank founders have a tough decision to make in this regard.

Agile Fintechs

Dealing with the core banking question is where the new breed of fintech banks can be very agile. Neobanks are examples of this. These digital only banks provide a range of convenient services, often at low cost, to retail clients and businesses alike.

Neobanks do not write their own code, but instead purchase templates based on selected fintech products that have been created across the world. These products often have established traction with users, making the choice to copy them a less risky one.

The main challenge with the fintech approach is that their individual products and services often don’t cover a traditional bank’s full product line.

In this case, the answer is simple: new fintechs can create an ecosystem of different fintech products to match the full product line of a bank. This approach can be a viable one for many new banks.

Digital-Only Banks vs. Traditional Banks: Which Model Fits You?

Capital drives innovation across a variety of industries. Banking is a great example, as evidenced by the emergence of online-only banks. There’s no shortage of options for this investment bank generation, but is this new approach right for a first-time banking project?

Well, we’ve touched on the importance of planning and the challenges that banks face, so let’s dive into another choice you make when you start a bank: digital or traditional. First things first, the benefits of an online bank are clear:

- Minimal cost of location setup and maintenance;

- Smaller staff numbers;

- Ability to extend services to new markets with less investment;

- Faster client communication and service.

But, as you know, those who open a bank also face issues, which for online banks come in the form of:

- Potential complications in legal compliance;

- High technological expectations;

- Severe competition;

- Demand for 24/7 service by clients.

These will certainly stand between you and a profitable banking venture. Yet, to be fair, traditional has its own pros and cons. Maintaining branches across cities, states, and countries can be incredibly costly. Staffing them, not just in terms of budget, but finding the right specialists, doubly so. However, you get the advantage of going down a well-trodden path, knowing exactly what mistakes to avoid.

In short, digital is good if you want to work on a budget while running a lean company with rapid development and constant customer outreach. Meanwhile, traditional banks help establish trust with clients, spread brand awareness through the branches, and lower potential risks.

The final decision will obviously involve weighing these pros and cons as they apply to your own resources and desired brand image. For example, a bank that seeks to sell its services as forward-thinking and modern is likely better off with a digital-only model. Meanwhile, those seeking to capture the older clientele might want to avoid going all-in on online.

Starting a Bank: Understanding the Regulatory Environment in 2024

2023 proved to be a consequential year for US banking. In a week, two of the largest financial institutions in America — Silicon Valley Bank and Signature Bank — went from managing billions of dollars to being in resolution. Further down the line, First Republic Bank had to be placed into receivership after failing to heed FDIC concerns for years, whereas dozens of small and midsize banks reported record levels of deposit and liquidity stress. In response to these events, bank regulators are sharpening their focus on perceived regulatory weaknesses this year in a number of ways, including:

Risk Management and Regulatory Supervision

The aftermath of 2023’s bank failures exposed significant weaknesses in the intensity of regulatory supervision over the previous decade. In 2024, tighter scrutiny on how banks manage financial risk is expected to be a focal point. Consequently, individuals thinking about how to start a bank will have to cooperate closely with regulators to report liquidity, understand potential risks, and devote more resources to thorough examinations, whereas super regional banks should prepare to address critical supervisory issues in much tighter timelines.

Crypto and Digital Finance

In 2024, banks partnering with fintech or engaging in activities involving blockchain and cryptocurrency will face heightened probes from regulators. Thus, founders interested in starting a bank business need to understand how digital assets work and how they fit into existing legal frameworks so their banks can adopt these emerging technologies without crossing legal boundaries.

Basel III Endgame

Basel III Endgame is a directive aimed at applying the strictest risk-based approach to more banks by reducing the threshold from $700 billion to $100 billion in assets. By regulators’ estimates, this would entail a 6 to 19% increase in capital requirements compared to current standards.

Banking Licensing

Starting a bank is a lengthy process that may span up to a year or more due to heavy regulation and the need for approval from various regulatory authorities. Obtaining approval for a state or federal charter, then securing deposit insurance from the FDIC, and potentially undergoing further examinations from the Federal Reserve are all crucial in this process. On one hand, any state can grant its charter. On the other hand, only the Office of The Comptroller of the Currency may issue you a national charter. If you manage to secure a charter, the next step is obtaining deposit insurance from the Federal Deposit Insurance Corporation (FDIC). But bank regulation doesn’t end with licenses. Most banks are required to subscribe and devote resources to several additional regulations like Know Your Customer, reporting standards, and company good practices i.e. taxation, investor transparency, and anti-money laundering, among many others. To evade these regulatory hurdles, many prospective banks don’t acquire their licenses; rather, they operate under the license of established banks. The downside to this is that they can refer to themselves only as fintech companies, not banks.

Capital Requirements

Founders or board members of the prospective bank must prove to regulators that they have enough capital to support its operations, risk profile, and future growth and that the bank can withstand economic downturns and initial losses.

These capital requirements aren’t dictated by guesswork. Rather, regulators will consider the market you want to enter and then indicate an adequate amount of capital for operating in that market. That said, the average capital requirements for a bank are significant. According to OffShoreCompany.com, you’ll need $500,000 to $1 million in startup costs and $10 to $30 million in capital to start a bank business.

Underfinanced banks are more inclined to take shortcuts, so declaring lower capital decreases the likelihood of winning FDIC deposit insurance. However, if you do not have the required capital by the time you meet regulators, your proposed bank may be allowed to proceed with a realistic strategy for raising capital in your business plan. Building off this point, prospective bank founders should be aware that fundraising is an ongoing activity. Therefore, you shouldn’t wait until you’ve secured all funding before approaching regulators. Oftentimes, obtaining banking licenses is enough to secure funding from investors who can guarantee your operation is serious, thus fastening your time to market.

Risk Management Framework for New Banks

When you start a bank, you implicitly agree to take on quite a bit of risk, as it’s a competitive industry that requires substantial finances to even break into, and the field can be volatile to boot. However, managing this risk is also a natural part of running a banking institution, so let’s talk about how you can do that.

Experts have said that this decade and the beginning of the next will be marked by deepening and broadening regulations, requiring banks to take on greater responsibility. Or, in other words, more risk. Having capital control nowadays comes with additional requirements, including liquidity levels, funding sources, leverage rate setting, and more. Tracking these figures is essential and, thankfully, can be automated with excellent analytics tools.

Another major risk area stems from the extent to which the financial market has truly become interconnected. No investment bank is an island anymore, and you can be affected by cyberattacks that don’t even target your business. What we mean is that disruptions in your partners’ security protocols can and will negatively affect your bank, making it necessary to take new precautions.

Combine that with what specialists call “contagion risk”, where the negative movements of markets in the bank’s jurisdiction can harm the bank’s own finances and profitable future. This is particularly crucial if a bank is designated as a global systemically important one. In that scenario, the institution is subject to extra regulations and surcharges.

It’s pretty much impossible to open a bank without using AI in some capacity nowadays. Therefore, you should also be mindful of the risks associated with model use and ways those models can help alleviate them. The core points from expert reports can be summed up as:

- Conduct regular performance monitoring;

- Assess models for bias and seek to correct it;

- Track analytical data and verify it;

- Set up third-party audits.

Starting a Bank: Building Your Banking Infrastructure

New banks rely on multiple hardware and software systems to carry out their operations.

Physical and Software Technologies

Banking hardware comprises phones, tablets, and computer systems used by employees and sometimes customers to conduct business operations. These include cash dispensers, automated teller machines, point-of-sale terminals, card readers, and physical security devices for multi-factor authentication, similar to cold crypto wallets.

Meanwhile, core banking software is the backbone of every modern bank business. These applications facilitate day-to-day functions, such as processing deposits and withdrawals and updating accounts and records.

Examples of core banking applications include business intelligence software:

- Artificial intelligence and Large Language Models used to mine insights from vast amounts of data;

- Customer Relationship Management (CRM) software used to manage customer experiences;

- anti-money laundering and fraud detection software used to identify and prevent financial crimes;

- loan automation software that streamlines the loan application and approval process.

As a new bank founder, you’ll also need core banking software for efficient record-keeping of client accounts, monitoring inflows and outflows, and report generation to satisfy regulations. By leveraging innovative solutions when starting a bank, the organization you build will be able to automate tedious processes, save costs, inform business decisions, and improve the customer experience, all of which drive profits and consistent growth.

Internal Processes and Compliance

Approved banks have to set up robust internal processes to ensure legal compliance and operational efficiency.

AI and Machine learning

Regulatory compliance is a critical function that costs 50% of banks 6-10% of their revenue, on average. However, the rise of artificial intelligence and machine learning algorithms is set to revolutionize the development of internal banking processes by automating repetitive tasks, identifying suspicious activity, analyzing vast loads of data, and offering real-time insight into everyday decisions.

Staff

When you think about how to start a bank, understand that no financial institution can be run by a sole founder. Even the smallest fintechs tend to have up to ten personnel, whereas most banks have 20 or more full-time employees, including accountants, personal bankers, loan originators, investment consultants, internal auditors, and other roles. However, beyond operational staff, you’ll also need to account for an FDIC-approved management team. The members of this team should share vast knowledge of banking services and financial markets to ensure effective leadership and decision-making.

Security

On the one hand, banks with physical locations must consider the costs of essential security resources like human guards, vaults, electronic security systems, cameras, and armored vehicles for cash delivery. On the other hand, fintechs or digital banks must invest in robust cybersecurity measures to keep their customers’ money safe and secure. With the various infrastructures brick-and-mortar banks need, it makes sense to think digital banks have it easier in terms of security costs. Well, think again. This study reports that the average cost of a data breach cyberattack on banks was $5.9 million in 2023, proving the cost of not complying with updated security protocols.

Conclusion

Starting a bank is a difficult process. Any new founder needs to be aware of the steep challenges they will face.

Banks are the lifeblood of an economy and are rightly safeguarded by regulators from failure. Founding teams must be prepared to face deep scrutiny of their backgrounds and their future intentions.

There are many key decisions to be taken when founders decide what type of bank they will open and what market segment they will serve.

Partnering with an established player in a key area such as the core banking system can remove much of the trouble and risk of going it alone.

Subscribe

Thank you!

Get ready! You will receive handpicked content right to your inbox.